Believe it or not, if you’re a working professional, there might be a time when you’ve at least had that thought.

What would happen to my family and loved ones if something happened to me?

Life can be a pretty unpredictable beast. Things can happen and no matter how much you earn, there will be no one who’ll take care of your family after you’re gone.

This is why getting life insurance might just be the best and most important decision of your life.

In this blog post, we will learn everything there is to know about life insurance, the different types, and how you can pick one that is good for you. Also learn about Types Of Life Insurance by reading this article.

The Importance of Life Insurance

Since the life insurance is promoted by both government and companies over time, there must be some reason behind it. So, the following are some reasons why life insurance is necessary for you too:

Financial Security for Family

Let’s say you are the only earning member of your family. So, what will happen if you get into an unfortunate situation that might end your life. In such cases, a life insurance can be the last financial support that can help out your family behind your back.

Child’s Education

The money invested in your insurance plan can be later used to ensure your child’s education. Your child’s education is the next best option where your term insurance money can be used. So, start investing from today, and secure your younger generation’s future.

Retirement Planning

What if we tell you that your life insurance can also be taken into use after your retirement. Yes, various schemes in numerous plans ensure that you keep getting a proper inflow of cash even when you have spent all the years working in a job or a business.

Tax Benefits

Under section 80C & section 10(10D) of the Income Tax Act, life insurance are treated as an exception. How so? Well, premiums paid towards life insurance policies are resulted to tax deductions. But what if the beneficiary receives death benefits? Well, they are non-taxable too.

Inflation Protection

On average, inflation rate ranges between 6-9%. This means, your money keeps reducing its value over a period of time. Hence, life insurance help you beat that loss with find value in ULIPs that can be increased with time. Ultimately, a significant amount of your money is already inflation-adjusted.

DID YOU KNOW?The death benefit payout for most life insurance is tax-free in most countries. This means if something happens to the policyholder, the beneficiaries will usually get the full sum insured amount with any tax deductions.

What are the Different Types of Life Insurance?

You know, life insurance is not the pay-and-you’re-done kind of thing, there are many different types of life insurance options available to you. And they each have a different type of coverage goal.

Term Life Insurance

If you’re on a budget and want a plan that you can afford, your best bet would be to get a term life insurance plan.

It is the purest form of life insurance as there is no saving or profit to be made from this policy. And if you compare it with other plans, you’ll find that it is also the cheapest option out there.

But there is a limit on the time this policy will be protecting you and if you want to extend the time you’re protected, you need to renew the plan or buy a new one.

Permanent Life Insurance

While any kind of coverage is good, many would like to have a plan that will have their back for life.

This means that unless you stop paying your premiums, or surrender the policy, you’ll be pretty much covered until death do you part.

The ULIPs Policy

ULIPs are one of the most unique styles of life insurance and if you have a penchant for taking risks then this plan is for you. T

It is a plan that hedges some of the sum insured amount of your as part of an investment in equities and markets.

Endowment Plan

This plan is a mix of both a good insurance plan and a savings account. Endowment plans can be a great investment for those who have outlived their insurance plans.

While it will cover you through the protection period, it also works as a kind of a savings account. So, once you get to maturity, you have the option of getting a little bit extra cash with all your premiums to date.

Child Plan

Child plans are for parents who worry about their children’s future. This plan has a unique payout system that is different from other life insurance plans too.

So, if you’re a parent worried sick about what would happen to your child if something happened to you, then this is the plan you’re looking for.

Retirement Plan

Living till you’re old and retired is like a dream for many and if you’ve gotten to this point, congratulations, you’re one of the few that make it to this point.

But, if life has taught you anything, it is that this is the time that you’ll need money the most.

When you’re old and retired, there is not much that a plain old life insurance can do for you. This is why the retirement plan was made.

This plan helps you build a trust fund for the time you retire.

This means that after you’ve ]left your job, the plan will give you a little bit of cash to tide you over and if something happens to you, your spouse or beneficiary will get the lump sum so they can be financially independent in their golden years.

Do you know that some insurance companies would not sell you insurance if you’re not healthy?

We recommend that you get your health checked regularly. You can also check your BMI using the BMI calculator for men through this link.

How Do You Pick The Right Insurance Plan For You?

You might be thinking, with so many options and types available, which one do you really pick? It’s not like there’s a one-size-fits-all kind of insurance plan out there you know.

If you’re as confused as most people are by this point, there is a simple way to narrow down your options. Here are the steps you need to follow:

See What Your Insurance Advisor Has To Say Insurance advisors are the pros in the field and they deal with insurance on a daily basis. Ask them what you’re expecting from your policy.

How Much Money Do You Really Need You need insurance that will cover all the basics and necessities of your loved ones for some time after your death. Calculate everything and then add some to find out how much you’ll need.

Compare All the Plans If you have decided on what you want and how much you want, now is the time to compare which plan you need to get. You need to pick one that ticks all the boxes on your checklist.

Pick a Premium Amount that You Can Realistically Afford Insurance plans can be cheap or expensive depending on the things you need from them. And remember you need to pay your insurance company an amount to keep your insurance active. So, this is why you need to decide on an amount that you can afford but will cover all your family finances for a couple of years.

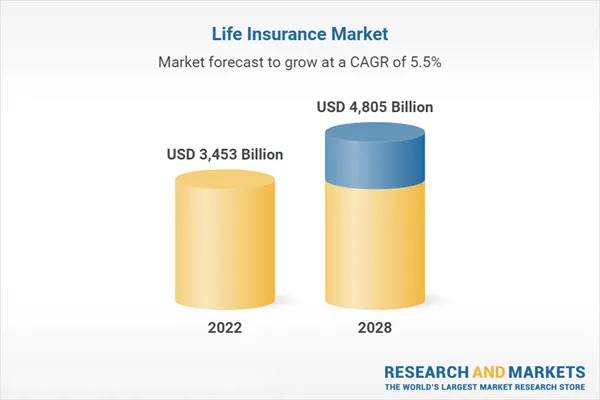

The global life insurance market was capped at $3.66 trillion in 2023 and is supposed to grow to $4.8 trillion by 2028. It will grow with a CAGR of more than 6% during the period.

TL;DR: The Conclusion

Life can be full of ups and downs and you can’t tell what will happen next. You need a way to protect your loved ones from the uncertainties in life, and this is why most people buy life insurance these days.

But simply getting a random insurance plan is not that great an idea, you need to take a look at the different plans available and look for things that you need from your plan. And if things get confusing you can always count on a professional to recommend the best plan for your needs.

Thanks for choosing to leave a comment. Please keep in mind that all comments are moderated according to our comment Policy.

About Us

MediaPract is dedicated to providing the latest national and international news, product launches, tech events, emerging tech, insightful topics, and all things tech and social media. With diverse perspectives, we have a team of experts, freelancers, independent journalists, and stringers working behind the scenes to source, research, and publish significant and trending news from every corner of the world.

At MediaPract we firmly believe in delivering objective information, preventing our readers from being influenced by preconceptions. Media Pract is looking forward to your participation in fostering a strong community and promises to deliver a wide range of news stories and features to cater to a diverse audience.